by Roger Caiazza

A case study on the challenges of controlling CO2 emissions.

The Regional Greenhouse Gas Initiative (RGGI) is a carbon dioxide control program in the Northeastern United States. One aspect of the program is a program review that is a “comprehensive, periodic review of their CO2 budget trading programs, to consider successes, impacts, and design elements”. On September 26, 2023 the RGGI States hosted two webinars describing technical modeling & analyses that examined the electricity market, emissions, and economic impacts of changes to RGGI. This post describes the disconnect between the results of RGGI to date relative to the expectations in the RGGI Third Program Review modeling that I addressed in my comments to RGGI.

Background

RGGI is a market-based program to reduce greenhouse gas emissions. According to RGGI:

The Regional Greenhouse Gas Initiative (RGGI) is a cooperative effort among the states of Connecticut, Delaware, Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island, Vermont, and Virginia to cap and reduce power sector CO2 emissions.

RGGI is composed of individual CO2 Budget Trading Programs in each participating state. Through independent regulations, based on the RGGI Model Rule, each state’s CO2 Budget Trading Program limits emissions of CO2 from electric power plants, issues CO2 allowances and establishes participation in regional CO2 allowance auctions.

More background information on cap-and-trade pollution control programs and RGGI is available from the Environmental Protection Agency and my RGGI posts page. Proponents of these programs consider them silver bullet solutions. However, I agree with Danny Cullenward and David Victor’s book Making Climate Policy Work that the politics of creating and maintaining market-based policies for Greenhouse Gas (GHG) emissions “render them ineffective nearly everywhere they have been applied”.

Third Program Review

The RGGI participating states hosted two public meetings on September 26, 2023, to discuss updates on the Third Program Review and electricity sector analysis. Meeting materials included the following: Meeting Agenda PDF; Presentation Slides PDF; Topics for Consideration PDF; Draft RGGI Emissions Dashboard ArcGIS Dashboard; RGGI Emissions Dashboard Draft User Guide PDF; Meeting Recording – Session 1, Meeting Recording – Session 2 and Draft IPM Matrix Case Results XLSX.

The RGGI States contracted ICF to analyze the different scenarios to inform the options for future RGGI. ICF has a proprietary model, the Integrated Planning Model (IPM©), that has been used by the RGGI States since the inception of the program and which EPA uses to evaluate many of its control policies. According to ICF:

ICF’s Integrated Planning Model provides true integration of wholesale power, system reliability, environmental constraints, fuel choice, transmission, capacity expansion, and all key operational elements of generators on the power grid in a linear optimization framework. The model captures a detailed representation of every electric boiler and generator in the power market being modeled.

In March the RGGI States explained that they planned to use IPM to evaluate several issues. One problem is “fluidity of state participation”. Nine states have been members of RGGI since its inception. New Jersey was a charter member, got out, and now is back in; Virginia was in but is now getting out; and Pennsylvania is trying to get in but participation has been stalled by litigation. RGGI planning must address climate and complementary energy policies that will dramatically impact electricity load such as electric vehicles and EV infrastructure, electrification in the building sector, and aggressive energy efficiency efforts. A major concern of the program review was allowance availability so the decarbonization timeline for the electricity sector was considered. This is complicated because participating State timelines vary, implementation of offshore wind deployment affects decarbonization rates and grid-scale battery storage deployment, duration, and supply certainties affect the outcomes.

The September 26 webinar described three key observations from the modeling results:

- Modeling shows how current state decarbonization and renewable requirements can significantly reduce emissions;

- Federal incentives for clean energy have the potential to rapidly transform the RGGI region generation mix; and

- Scenarios modeled to date show relatively low allowance prices compared to the ECR/CCR price triggers in the Model Rule

The RGGI States have not proposed their plans for the Third Program Review. The modeling observations support the idea that the RGGI allowance availability can be made more stringent. So much so that the modeling plans changed from the spring to add a more stringent trajectory to reach zero emissions by 2035 rather than just looking at a zero emissions by 2040 trajectory. My comments addressed these key observations .

I will summarize my concerns below but first it is necessary to review RGGI results to date.

RGGI Results to Date

There is an unfortunate disconnect between the results of RGGI to date relative to the expectations in the Third Program Review. During the September 26 meeting the explanation of cap-and-trade systems stated that “States reinvest the proceeds in decarbonization and other programs to deliver benefits to their communities.” What was missing was any mention of the efficacy of those investments relative to the emission reductions observed.

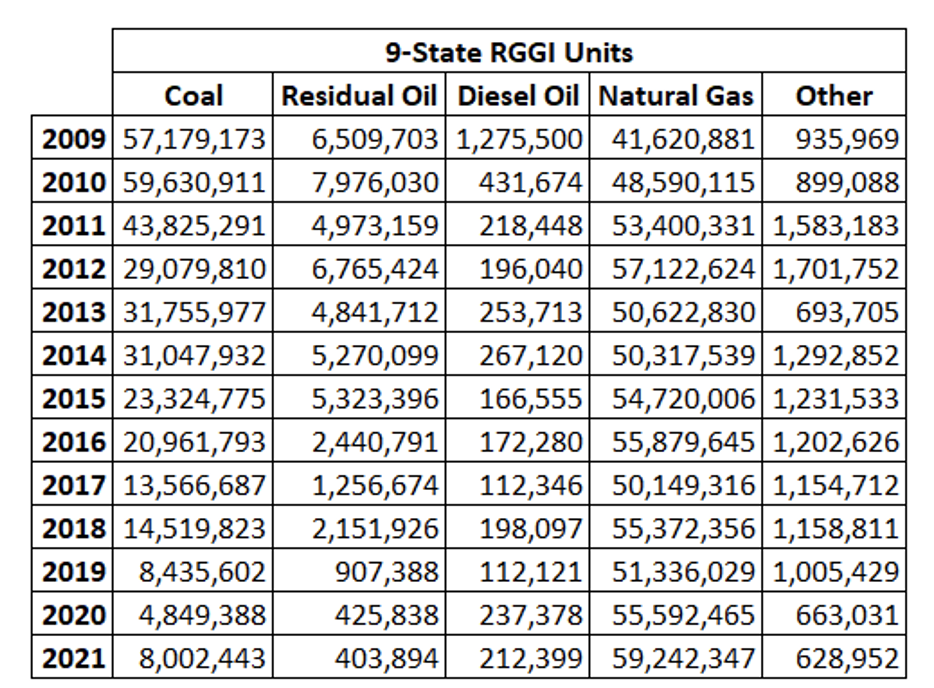

The primary cause of the observed RGGI emission reductions has been the fuel switch from coal and residual oil to natural gas. Table 1 lists the emissions by fuel types for the nine RGGI states that have been members since the start. I believe that RGGI had very little to do with these fuel switches because fuel costs are the biggest driver for operational costs and natural gas was cheaper. The cost adder of the RGGI carbon price to date has been too small to drive the conversions from coal and oil to natural gas.

Table 1: RGGI Program Unit CO2 Emissions (tons) by State and Year

RGGI sources within the nine-state region have already implemented most of the coal and residual oil fuel switching opportunities available so this control strategy will be less impactful in the future. For example, in New York coal-fired electric generation has been banned and the remaining units that burn residual oil primarily run to only provide critical reliability support so their emissions are not expected to change much from current levels. In the future, RGGI affected source emission reductions will rely on the displacement of natural gas fired units with wind and solar zero emitting sources.

The 2021 investment proceeds report released on June 27, 2023 provides insight into the success of RGGI investments as an emission reduction tool. The report breaks down the investments into five major categories:

Energy efficiency makes up 51% of 2021 RGGI investments and 55% of cumulative investments. Programs funded by these investments in 2021 are expected to return about $418 million in lifetime energy bill savings to more than 34,000 participating households and over 570 businesses in the region and avoid the release of 2.3 million short tons of CO2.

Clean and renewable energy makes up 4% of 2021 RGGI investments and 13% of cumulative investments. RGGI investments in these technologies in 2021 are expected to return over $600 million in lifetime energy bill savings and avoid the release of more than 1.7 million short tons of CO2.

Beneficial electrification makes up 13% of 2021 RGGI investments and 3% of cumulative investments. RGGI investments in beneficial electrification in 2021 are expected to avoid the release of 370,000 short tons of CO2 and return nearly $164 million in lifetime savings.

Greenhouse gas abatement and climate change adaptation makes up 11% of 2021 RGGI investments and 8% of cumulative investments. RGGI investments in greenhouse gas (GHG) abatement and climate change adaptation (CCA) in 2021 are expected to avoid the release of more than 10,000 short tons of CO2 and to return over $20 million in lifetime savings.

Direct bill assistance makes up 14% of 2021 RGGI investments and 13% of cumulative investments. Direct bill assistance programs funded through RGGI in 2021 have returned over $29 million in credits or assistance to consumers.

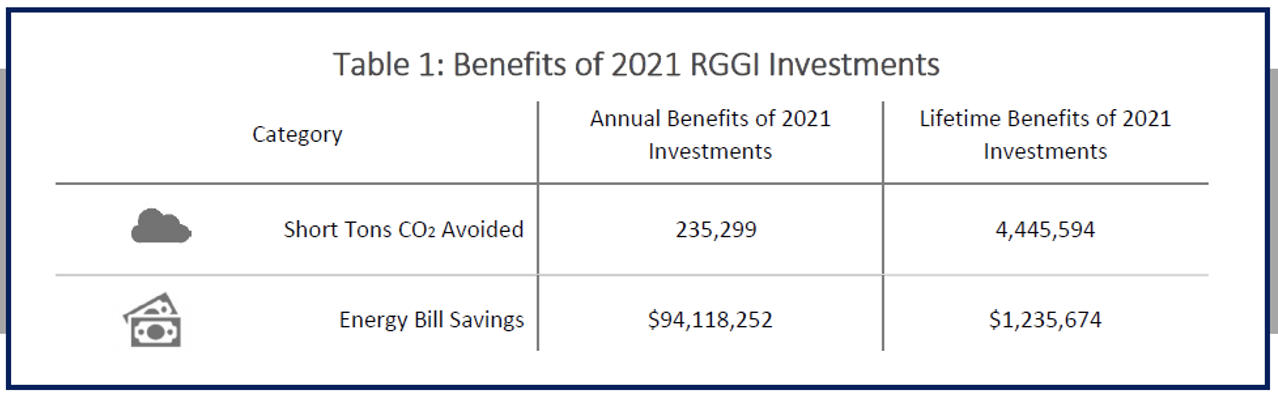

There is an important caveat to the emission reductions reported in the report. The RGGI compliance metric is annual emissions and the above quote lists the lifetime emission reductions. The sum of the lifetime emission reductions from the 2021 investments is 4.38 million tons but the annual emission reductions due to RGGI investments were only 235,299 tons (Figure 1). The 9-state allowance allocation annual reduction in 2021 was 2,275,000 allowances so RGGI was only responsible for around 10% of the emission reductions required.

Figure 1: Table 1 from the 2021 investment proceeds report

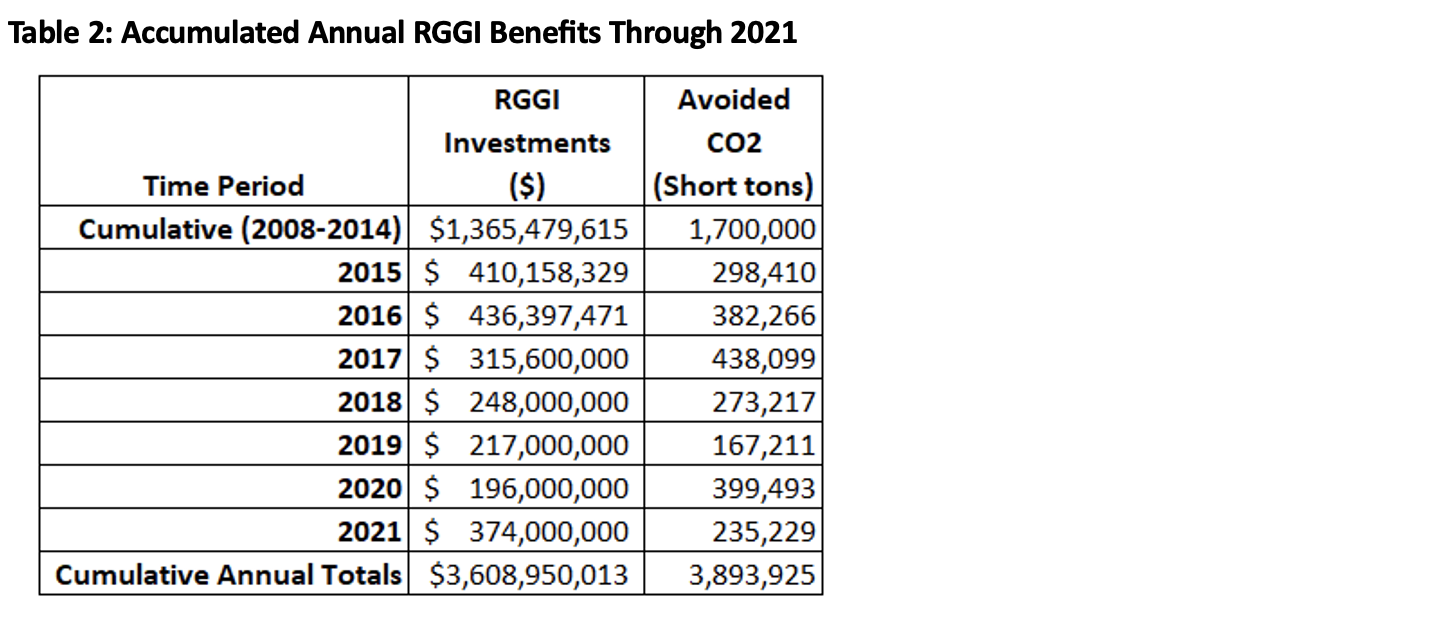

The results in 2021 are consistent with historical observations. To make a comparison to the CO2 reduction goals I had to sum the annual values in the previous reports because RGGI does not report the annual RGGI investment CO2 reduction values accumulated since the beginning of the program. Table 2 lists the annual avoided CO2 emissions generated by the RGGI investments from previous reports. The accumulated total of the annual reductions from RGGI investments is 3,893,925 tons while the difference between the three-year baseline of 2006-2008 and 2021 emissions is 58,334,373 tons. The RGGI investments are only directly responsible for 6.7% of the total observed annual reductions over the baseline to 2021 timeframe!

Table 2: Accumulated Annual RGGI Benefits Through 2021

Dividing the total RGGI investments by the total tons reduced provides the cost per ton reduced. The cumulative RGGI investment cost effectiveness is $927 per ton reduced. That is far more than the Resources for the Future Social Cost of Carbon estimate of $185 per ton and indicates that costs exceed societal benefits.

Concerns with Results – Recommendations are highlighted in bold

The September 26 RGGI meeting observed that “Modeling shows how current state decarbonization and renewable requirements can significantly reduce emissions”. There is a unique aspect of the Third Program Review modeling process that has not been available previously. There are two independent modeling projections of the New York electricity system resources necessary to meet a zero-emission target by 2040. The New York Independent System Operator (NYISO) has evaluated scenarios that project the resources necessary to achieve the New York Climate Leadership and Community Protection Act goal of a zero-emissions electricity generating system by 2040. New York’s Scoping Plan was guided by an Integration Analysis that modeled the transition. Comparison of those projections with the Integrated Planning Model (IPM) projections enables a check on how these requirements can reduce emissions using different methodologies.

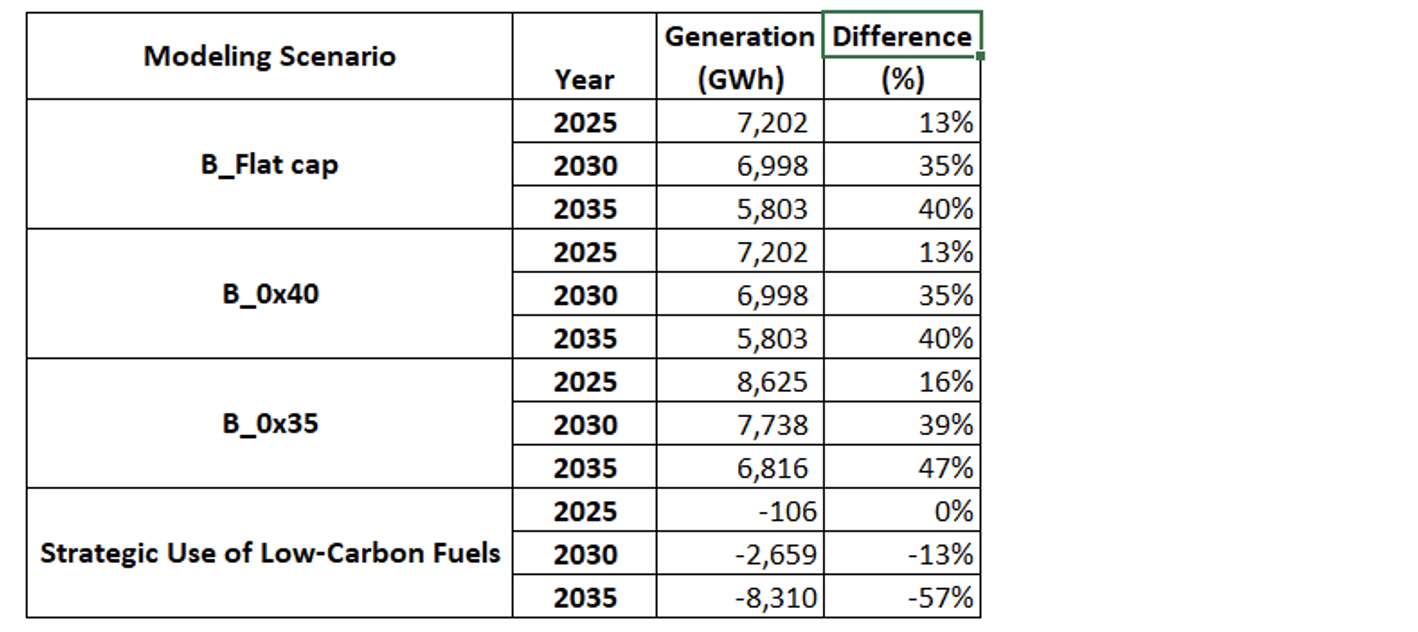

It turns out that there are significant differences between the RGGI IPM modeling and the other analyses. The most glaring difference between the RGGI IPM modeling of New York and the New York analyses is the generation fossil-fuels sector (Table 3). The table subtracts the NYISO Resource Outlook Scenario 1 projected generation from the RGGI IPM modeling allowance supply scenarios for Assumption Set B and Integration Analysis Scenario 2. The percentage difference shows that the IPM projects substantially more generation than NYISO and the Integration Analysis.

Table 3: Fossil Resource Sector Difference in Generation (GWH) Between the NYISO Resource Outlook and the RGGI IPM and Scoping Plan Integration Analysis Strategic Use of Low-Carbon Fuels Scenario

Because RGGI affected source emissions are so strongly correlated with operations these higher operating rates mean that the RGGI IPM modeling projects lower fossil-fired emissions than either model. In Table 4 I estimated New York CO2 emissions by multiplying these projected generation differences times the 2022 calculated CO2 emission rate per MWh. In the NYISO Resource Outlook column the emissions are relative to those scenario differences. Similarly, the emission differences in the Integration Analysis are relative to the Scoping Plan projections. IPM underestimates the fossil sectors emissions significantly.

Table 4: Fossil Resource Sector Difference in Projected CO2 Emissions (tons) Between the RGGI IPM and NYISO Resource Outlook and Scoping Plan

The RGGI States chose not to include any allowance supply numbers so I was forced to make my own estimates to determine the significance of these emissions. I projected allowance availability using a linear interpolation between 2023 allowance allocations and zero by 2035 and 2040. For the zero by 2040 allowance supply scenario, the 2030 emissions difference represents 27% of my estimated allowance allocation. For the zero by 2035 allowance supply scenario, the 2030 emissions difference represents 42% of my estimated allowance allocation. This suggests that this modeling difference needs to be reconciled to determine its impact on the RGGI State allowance allocation trajectory proposal.

There is another issue associated with the modeling results. The ICF description of these modeling results notes that “due to the stringency of the program after 2040, the model shows an over-compliance of emissions in the early years (2025-2030) and banking of those allowances for when the cap is reduced in 2035 and beyond. “ This is an artifact of the perfect foresight methodology of IPM and, I believe, is unlikely to occur.

I think this is wrong because the modeling approach claims affected sources “over-comply”. RGGI sources do not “over-comply” but rather acquire allowances to meet their compliance obligations with a slight surplus to ensure compliance My primary concern is New York and in New York sources that could fuel switch to natural gas have already done so. They cannot directly affect their compliance except by limiting operations. Thus, RGGI sources in NY are at the point where they must rely on renewable energy to displace their need to operate. This means that they only purchase the allowances they expect to use for their compliance obligations plus a small compliance cushion.

Based on the modeling description, IPM “perfect foresight” projects results over longer planning horizons than used in practice. I believe that affected-sources across RGGI treat the allowance requirements as a short-term, no more than a couple of compliance periods, compliance obligation. It is highly unlikely that most affected sources are making plans beyond short-term compliance periods so the idea that affected source would over-comply in early years for more stringent limits ten years ahead is incorrect. The open question is how does this affect the allowance trajectories. It might also account for differences between the NYISO and Integration Analysis projections. The best way to reconcile this is in an open public forum with the modeling groups.

The September 26 RGGI meeting also observed that “Federal incentives for clean energy have the potential to rapidly transform the RGGI region generation mix” but recent developments suggest that this may be overly optimistic. Renewable developments are struggling due to soaring interest rates and rising equipment and labor costs. Reuters describes two “procured” projects in the RGGI region that have been cancelled:

-

- On Monday, Avangrid (AGR.N), a U.S. subsidiary of Spanish energy firm Iberdrola (IBE.MC), said it filed agreements with power companies in Connecticut to cancel power purchase agreements for Avangrid’s proposed Park City offshore wind project.

- “One year ago, Avangrid was the first offshore wind developer in the United States to make public the unprecedented economic headwinds facing the industry,” Avangrid said in a release. Those headwinds include “record inflation, supply chain disruptions, and sharp interest rate hikes, the aggregate impact of which rendered the Park City Wind project unfinanceable under its existing contracts,” Avangrid said.

- Avangrid has said it planned to rebid the Park City project in future offshore wind solicitations. Also over the past week, utility regulators in Massachusetts approved a proposal by SouthCoast Wind, another offshore wind developer, to pay local power companies a total of around $60 million to terminate contracts to provide about 1,200 MW of power.

In New York, on October 12, 2023 the Public Service Commission turned down a request to address the same cost issues. Times Union writer Rick Karlin summarizes:

-

- At issue was a request in June by ACE NY, as well as Empire Offshore Wind LLC, Beacon Wind LLC, and Sunrise Wind LLC, which are putting up the offshore wind tower farms.

- All told, the request, which was in the form of a filing before the PSC, represented four offshore wind projects totaling 4.2 gigawatts of power, five land-based wind farms worth 7.5 gigawatts and 81 large solar arrays.

- All of these projects are underway but not completed. They have already been selected and are under contract with the New York State Energy Research and Development Authority, or NYSERDA, to help New York transition to a clean power grid, as called for in the Climate Leadership and Community Protection Act, approved by the state Legislature and signed into law in 2019.

Developer response to the PSC decision suggests that “a number of planned projects will now be canceled, and their developers will try to rebid for a higher price at a later date — which will lead to delays in ushering in an era of green energy in New York”. Karlin also quotes Fred Zalcman, director of the New York Offshore Wind Alliance: “Today’s PSC decision denying relief to the portfolio of contracted offshore wind projects puts these projects in serious jeopardy,”

These issues impact the proposed RGGI allowance trajectories based on the “potential to rapidly transform the RGGI region generation mix”. The IPM modeling projects significant emission reductions presuming that procured renewable energy projects will come on line consistent with the contracts at the time of the modeling. The two cancelled projects in New England total 2,000 MW and the threatened New York wind projects total 11,700 MW. Any projects delayed mean RGGI-affected source emissions will not be displaced as originally expected. If the allowance trajectory proposed does not account for this new information, then compliance will be threatened because affected sources have so few options available to reduce emissions. I recommended that a RGGI IPM modeling scenario be run to consider the effect of a delayed implementation schedule before finalizing Third Program Review recommendations. In fact, given the importance of renewable development on the emission trajectories it might even be appropriate to delay the timing of completion of this program review.

There is another consideration regarding feasibility. As noted above, the accumulated annual emission reductions due to RGGI investments is 3,893,925 tons and RGGI investments over the same time frame total $3,608,950,013 so the cost per ton avoided is $927. If the only source of future emission reductions were the result of RGGI investments, then RGGI allowance prices would have to equal $927 to get the necessary reductions. Of course, other investments will also reduce emissions but the RGGI States should consider cost considerations for the viability of renewable energy resources needed to get RGGI affected source emissions to zero. None of these models address this uncertainty.

The final observation noted at the September 26 webinar was that “Scenarios modeled to date show relatively low allowance prices compared to the ECR/CCR price triggers in the Model Rule”. Low allowance prices indicate that emissions are lower than the allowances auctioned so there is a surplus of allowances. My description of RGGI results to date noted that RGGI-affected sources have limited options to switch from coal and residual oil to natural gas. I expect that as the opportunities to switch fuels diminish that the allowance market will get tighter and allowance prices will go up. This could trigger the RGGI cost containment reserve. If allowance prices exceed predefined price levels, this RGGI feature will release additional allowances to the market. If the allowance trajectory is too aggressive and emissions do not decrease as expected because wind and solar do not come on line as planned or there is an abnormal weather year increasing load and decreasing wind and solar availability, then there could be a situation where there simply are not enough allowances available for compliance. The Cost Containment Reserve could prevent this from occurring. However, no scenarios with this feature have been modeled yet. I recommended that the RGGI States should model a scenario where the renewable implementation is delayed and the Cost Containment Reserve is employed.

Conclusion

I am afraid that the RGGI States are placing so much reliance on the IPM analysis results that they could propose unrealistic allowance reduction trajectories. It is naïve to treat any model projections of the future energy system without a good deal of skepticism because the electric grid is so complex and currently dependent upon dispatchable resources. Replacement of RGGI-affected sources with intermittent and diffuse wind and solar resources that cannot be dispatched is an enormous challenge with likely unintended consequences. Therefore, the results should be considered relative to historical observations.

I don’t see much indication that the RGGI States are considering the results of RGGI to date. I am leery of any model projections of this future system but I have much greater faith in projections by the NYISO because they are responsible for electric system reliability. I think there are significant differences between the NYISO projections and IPM. Until those differences are reconciled, I will be skeptical. Kevin Kilty summed up a rational approach to the use of model results that I fear the RGGI States will ignore:

“Beware. Expect Surprises. Expensive Ones”.

Personal Background

Roger Caiazza blogs on New York energy and environmental issues at Pragmatic Environmentalist of New York. He blogs about the RGGI program because he has been involved with it since its inception and nobody else apparently wants to critically review it. This represents his opinion and not the opinion of any of his previous employers or any other company with which he has been associated.

Thank you, Roger. You’re on top of it, as always.

Thanks

I don’t imagine that there is any provision to reevaluate the decision to reduce emissions if that decision was based on “settled science”. I do believe that that is the erroneous analysis upon which all this effort is based so likely all the effort and expense is wasted as well as lacking integrity and accuracy.

Integrity is never an aim in climate politics.

This scheme is just a backstop for when someone manages to over turn EPA’s unconstitutional strangle hold on energy policy via the “endangerment finding”.

They are attempting to rig the market at the state level so they can continue to destroy the energy market when SCOTUS clips the federal EPA’s vulture like wings.

So glad to be able to read actual science with actual data instead of “the sky is falling”. Just one question: How did Virginia get in this club of northeastern states? Seems odd to me.

Virginia had a Democratic governor who got the state into the program. He was thrown out of office and replaced by a Republican, who is (wisely) opting out of the program.

I know our Virginia Gov is trying to get out, but I am under the impression it is under review if he has the authority.

Geographically they adjoin Maryland but it is more about getting into the cool kids of a carbon cap and trade club. If they could get someone out west to join they would in a heart beat.

The whole RGGI program is a Democratic Party scam. There is virtually no reason to believe the effort will ever be pragmatically reviewed.

I wish I could argue with you but I can’t

The US is becoming increasingly more irrelevant in the world production of CO2, no? Accordingly, western academia has become totally irrelevant…

The last time those states got together, it turned out to be trouble for King George III. Looks more like trouble for NE USA this time.

We here in CT are very concerned that the political scamming of our grid is going to produce blackouts, shortfalls, & high prices. No reliability. Right now our energy assistance fund for the poor is pretty strapped. Of course we are not in good economic shape. In essence the body politic wants to assign our DEP the function of controlling emission standards but not the legislature. The aim is to protect democratic lawmakers from accountability particularly in cities. We find this very much a scam & I’m not sure it is constitutional. Bureaucrats not having accountability for decisions that clearly affect the circumstances of households. CT is not a smokestack state. It receives emissions from the jetstream flow. We just had a major wind project pull out because of cost. What irks the public is that we have the governor trying to take over consumer choice of products that are essential to a household. What about our opinion & our choice? What about the free market? Put up carbon capture if they are so concerned.

I feel the same way about New York. I wonder if when the inevitable blackouts come whether people will finally vote the clowns out.

Not totally convinced that ‘reducing emissions’ is the best policy decision. More likely that ‘increasing photosynthetic capacity’ is a cheaper, more sustainable and more natural way to balance carbon dioxide levels in the atmosphere.

I’m not against control of more overtly polluting emissions. Carbon particulates aren’t the greatest thing to end up depositing on polar ice, after all.

But there are vast areas of land the world over where better water retention and management can allow huge increases in photosynthetic capacity and this will accelerate over a few decades for less and less investment going forward.

Deforestation is a far, far bigger problem than ‘carbon dioxide emissions’ where global planetary health is concerned and it’s good to see increasing levels of sustainable reafforestation using integrated strategies of planting going on. Not to mention regenerative farmers managing their livestock better to transform pastures into rich carbon sinks.

I don’t think “increasing photosynthetic capacity” can deal with 100’s of millions of years worth of photosynthetically sequestered carbon (fossil fuels) being released over a period of a few centuries.

Did you run it on any numbers? “Few centuries” is not a number.

Very informative data table of fuels.

In the early 90’s I was vocal anti-coal, when NJ made it official state policy that coal was the only allowable fuel, and then NJ started siting new coal-fired plants in South Jersey (my backyard). I was saying instead go with nat gas.

Never thought I’d see (in my lifetime) the massive coal reduction we have witnessed in the data table.

In those days we had serious summer smog and ozone wafting into South Jersey from PA, OH etc. Like California, I am thinking RGGI had its start to reduce smog, and then Dems shifted the focus to CO2 reduction. We got off on a partisan witch hunt (Halloween reference) instead of something everyone could see the haze and need for cleaner air (cough, cough).

The world is burning more coal than ever. These 9 nutty states just don’t matter in the larger scheme of things.

The conversion away from coal was due to natural gas being a more economical fuel which was caused by fracking. If there is anything that gets a NY environmentalist more wound up than climate change it is fracking or possibly nuclear. Unfortunately those two fuels should be good enough but never will be.

Since being removed from this blog, I have moved to truth social.

On September 28, 2022 the average surface temperature of the sun began to rise, and the heat radiated to the black sky equaled that retained by the earth.

That was the beginning of the first little Ice Age of this, about 130,000 year large Ice Age.

Nature has all under control. Man can only pollute!!!!!

Something very big is brewing.

https://www.youtube.com/watch?v=S8CsR8DCp8Q

The oceans once super-heated the earth.

https://phys.org/news/2019-05-deep-sea-carbon-reservoirs-superheated.html

“It’s just mind boggling.” More than 19,000 undersea volcanoes discovered”

https://www.science.org/content/article/it-s-just-mind-boggling-more-19-000-undersea-volcanoes-discovered

Very faint spots on the solar disk.

https://www.sidc.be/SILSO/DATA/EISN/EISNcurrent.png

Winter in the US.

https://i.ibb.co/nsgDB6x/gfs-T2m-us-21.png

Blocking zonal circulation in the lower stratosphere in the North Pacific and Atlantic.

https://i.ibb.co/v468BLQ/gfs-t100-nh-f00.png

Pingback: State of the Regional Greenhouse Gas Initiative in the NE U.S. • Watts Up With That? - Lead Right News

Pingback: State of the Regional Greenhouse Fuel Initiative within the NE U.S. • Watts Up With That? - Finencial

Pingback: State of the Regional Greenhouse Gas Initiative in the NE U.S. • Watts Up With That?

One of the highest temperature anomalies in the US this year is currently observable in Texas. See our temperature anomaly map https://www.ventusky.com/?p=35.0;-99.7;5&l=temperature-anomaly-2m

Blocking the polar vortex in the North Pacific is a bad forecast for winter in the US. A lot of energy will be needed.

https://i.ibb.co/y5fyz2Z/gfs-t50-nh-f240.png

Quasi-biennial oscillation (QBO)

The QBO index is determined by the strength and direction of equatorial zonal winds in the tropical stratosphere. When the winds are in a westerly phase the index is positive and when in an easterly phase it is negative. A correlation between the strength of the jet stream across the North Atlantic and the QBO has been identified. A negative (easterly) QBO favours a weaker jet stream which in turn means a greater chance of cold spells during the winter months.

An easterly QBO is expected to continue through the winter. This is believed to increase the likelihood of a colder than average winter.

i.e., return on investment is negative- nothing more than a government-sponsored dead end detour to mass poverty.

Biden Alaska Oil Plan Seen as Major Threat to Future Drilling

Tighter rules risk viability of projects, ConocoPhillips warns

Proposal would impact even existing leases, industry fears

By Jennifer A Dlouhy

October 30, 2023 at 7:31 AM EDT

A century after the US set aside a broad swath of northwest Alaska to be used as an emergency oil supply, the Biden administration is pursuing changes that could make it impossible to harvest crude from new leases in the 23 million-acre site.

https://www.bloomberg.com/news/articles/2023-10-30/biden-alaska-oil-plan-seen-as-major-threat-to-future-drilling

Yes, more infantile fantasy ignoring both history and theory.

Natural gas is not dirty. CO2 is not pollution. The experiments have been done

We are not in control of CO2 (we produce less than 5% of the annual contribution to the atmosphere), and we note no effect on CO2 rise for 1929-1931 and for 2020, despite our decreases in output (30% in 1929-1931 and perhaps 17% of a much higher production in 2020).

No, not the slightest effect on the languid rise of CO2.

That latter greatly disappointed Arizona State University climate scientist Randall Cerveny who, unaware of 1929-1931, expressed his disappointment: “We had had some hopes that, with last year’s COVID scenario, perhaps the lack of travel and the lack of industry (that 17% drop in output) might act as a little bit of a brake. But what we’re seeing is, frankly, it has not.”

He is also unaware of the exponential decline in CO2’s GHG effect, discovered by Arrhenius, and the math is now correct (MODTRAN, U of Chicago). The next doubling to 800 ppm will increase its GHG effect by around 2%.

The sacrifices we are now making to the climate goddess are in vain. Perhaps self-flagellation will work. Those medieval processions were impressive.

We could eliminate our CO2 production entirely (hastening our demise) and it would not alter the risk of temperature rise in the slightest. That’s clear from history and from theory. Yes, the correlation of CO2 with temperature is good, as is the correlation of sex with marriage, and both demonstrate no causality, neither necessary nor sufficient.

As Klaus-Ekhart Puls has wisely said,

Scientifically it is sheer absurdity to think we can get a nice climate by turning a CO2 adjustment knob. Many confuse environmental protection with climate protection. it’s impossible to protect the climate, but we can protect the environment and our drinking water. On the debate concerning alternative energies, which is sensible, it is often driven by the irrational climate debate. One has nothing to do with the other.

Western circulation blocking. Stationary upper-level lows in the North Pacific and Atlantic and plenty of Arctic air in North America.

https://i.ibb.co/0f7M6Ky/mimictpw-namer-latest.gif

In a few days, snowfall will move from the Great Lakes to the northeast of the US.

so cool!

Wow, very cool article, how you were able to reveal and convey everything, I’m impressed with everything that was happening then. And these images are incredible, where you managed to find them, they are really rare. I’ve seen very little of this, only through the Depositphotos blog could I see something like this, and there were real treasures in terms of images. I’ve been living for so many years and working with photos for so long, this is honestly the first time I’ve seen such quality, taking into account the time. So I’ll be following your updates very closely, because this is the kind of content you can’t miss.